In June 2026, one of the world’s most prominent galleries announced that roughly fifty artists and estates would leave its programme. Fifty staff positions would also disappear. Pace Gallery’s contraction became an international story because it interrupted a deeply rooted ranking system within the art world: the larger the gallery, the more stable the careers attached to its name should become.

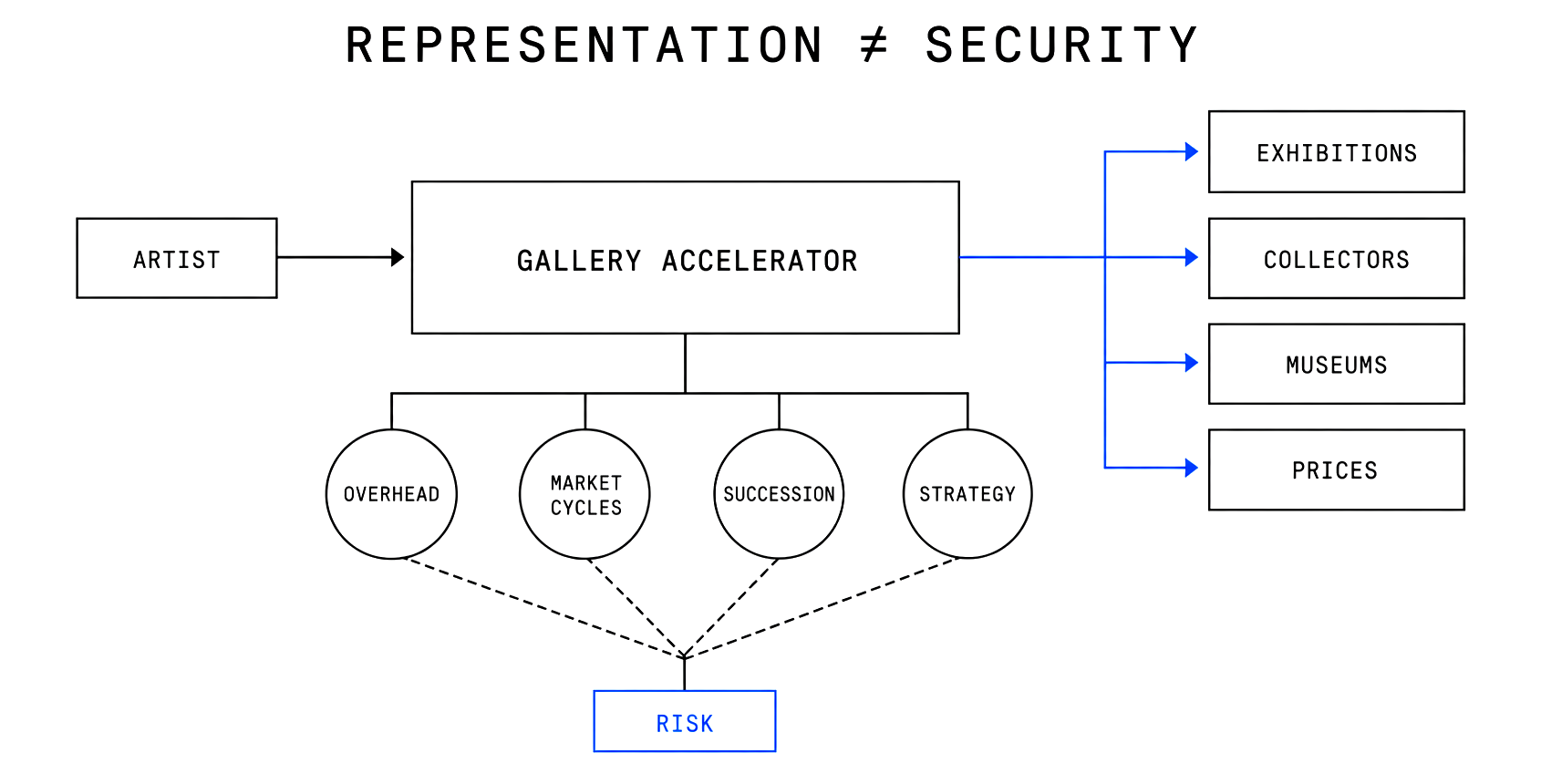

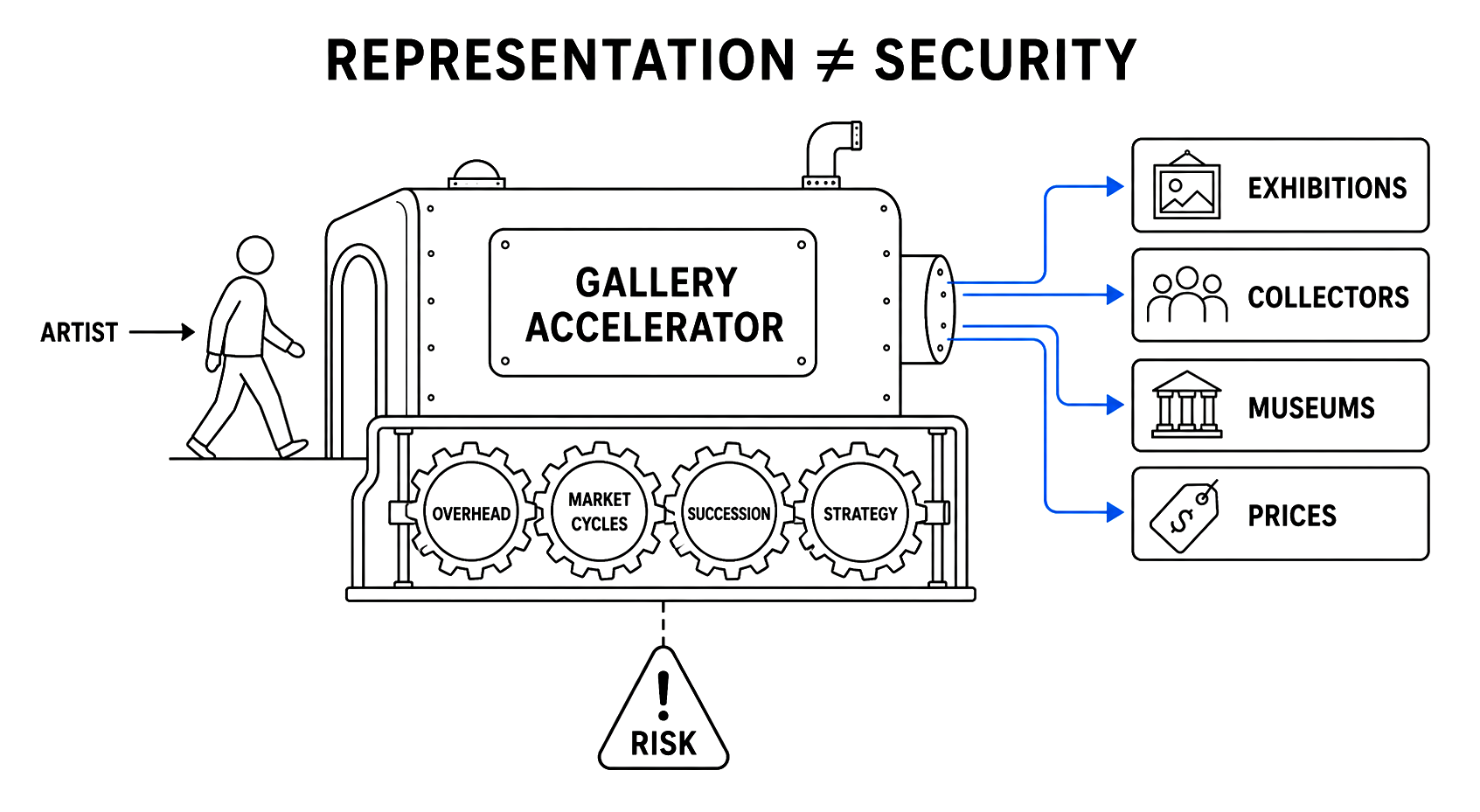

The actual geometry is less linear. A gallery can accelerate prices, exhibitions, acquisitions, institutional relationships, and access to collectors. It can support a practice for decades while protecting studio time from extensive commercial labour. Yet the gallery remains a business exposed to overhead, market cycles, internal succession, and strategic revision. Representation opens a distribution protocol; it never suspends risk.

Emerging artists often imagine representation as the moment when a career finally enters professional hands. From then on, someone else should sell, communicate, build reputation, produce exhibitions, and calibrate market exposure. The expectation contains genuine value and a dangerous degree of delegation. A gallery can extend the bandwidth of a practice, but it can rarely replace the ecosystem that makes that practice legible and durable.

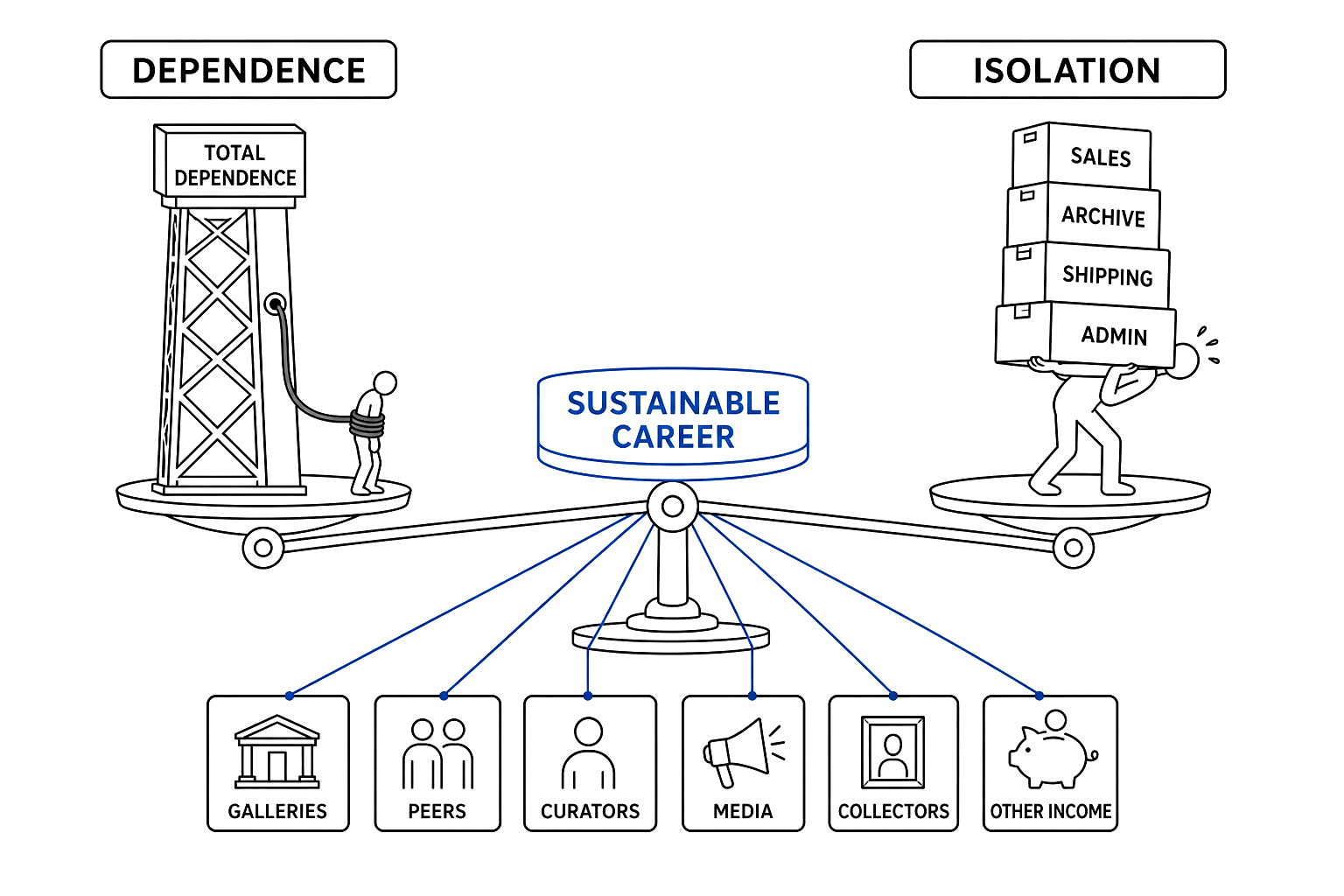

The opposite rhetoric creates its own illusion. Absolute independence treats every intermediary as extraction and assumes that platform reach can replace mediation. Sales, archives, negotiation, insurance, installation, writing, and relationship maintenance require time, expertise, and interface cadence. Total autonomy can become a second occupation that consumes the first.

A sustainable art career therefore develops between dependency and isolation. It needs capable galleries, independent spaces, curators, peers, media, collectors, and complementary income, while preventing any single node from becoming the entire parameter space. The artist’s task is to build a permeable subsystem in which every alliance increases the resilience of the others.

The Gallery as Accelerator

A good gallery performs labour that becomes visible mainly through its absence. It sustains conversations with collectors across years of hesitation, sequences which works reach which buyers, coordinates loans, verifies provenance, manages discounts, transport, insurance, and payments. Its distribution protocols can convert episodic attention into market memory.

The central value of representation often lies in selection. A gallery disciplines supply, protects price coherence, and prevents every momentary inquiry from becoming an inconsistent sale. It may forgo a quick transaction to place a work with a more suitable collection or institution. This commercial ranking sequencing has critical consequences because the destination of a work alters its future reading.

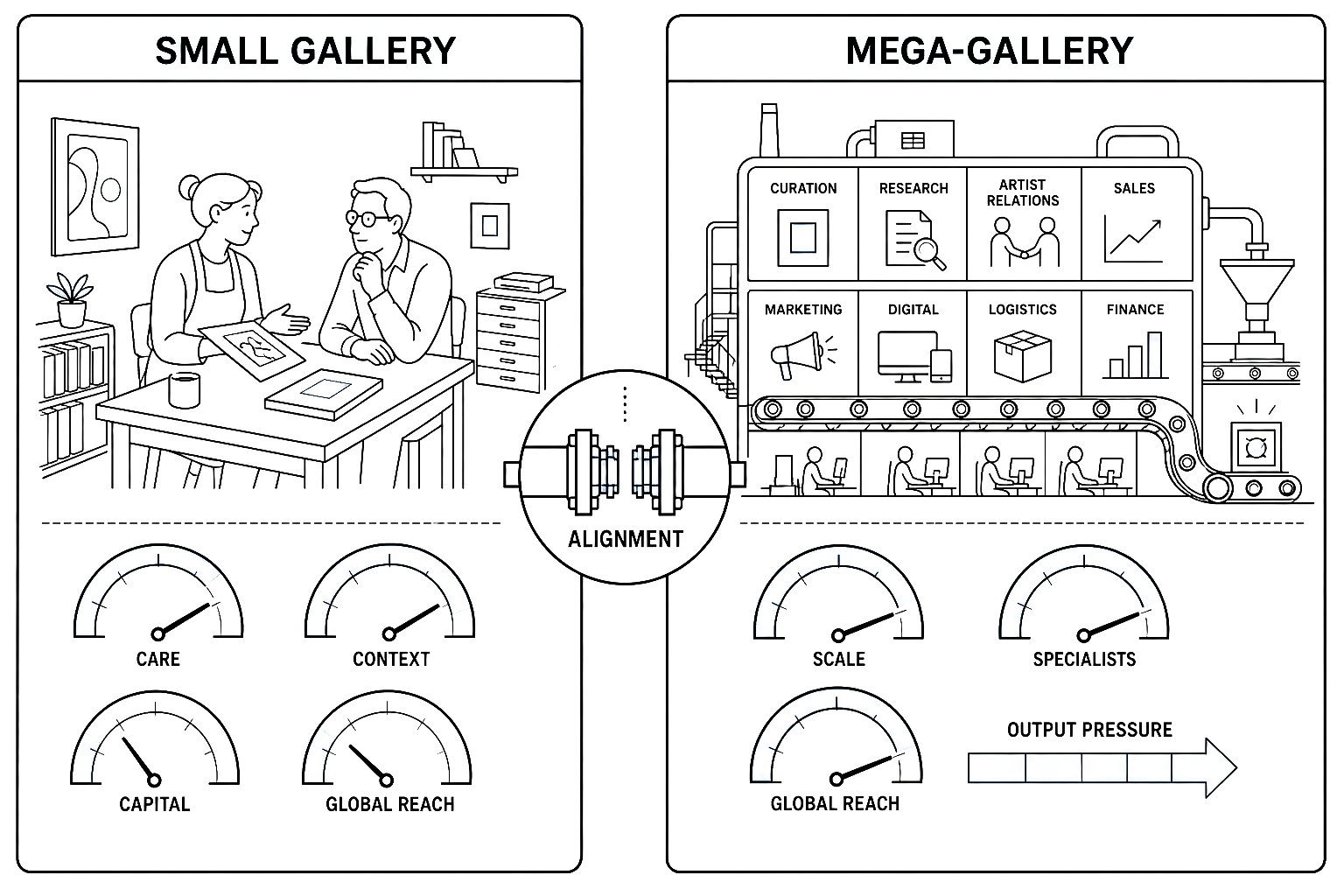

Scale expands the accelerator’s capacity. A mega-gallery operates international venues, press offices, archives, specialist departments, digital teams, and access to major fairs. It can coordinate the primary market, museum relations, publishing, and secondary-market governance. For the artist, this infrastructure removes certain frictions while introducing higher production cadence, greater expectations, and internal competition across a long roster.

A small gallery offers a different density. Its director may know every stage of production, sustain daily conversation, and build an audience slowly around work that remains commercially difficult. Capital reserves, international bandwidth, and the ability to absorb a failed fair are usually more limited. Proximity deepens care while economic exposure remains acute.

The useful question concerns alignment between the practice’s stage and the intermediary’s operational capacity. Prestige and suitability can diverge. An accelerator of excessive force may push price and output beyond the artist’s metabolism; an undercapitalised one may promise expansion it cannot finance. Representation works when both sides can govern its speed.

When the Name Leaves the Roster

Departure from a gallery feels like a judgement on the work, although organisational change often drives the decision. Leadership transitions, property costs, roster compression, mergers, succession, and market contraction reshape programmes. Marlborough closed in 2024 after almost eighty years; Kasmin and Clearing announced closures in 2025, while a new gallery absorbed parts of their programmes. Continuity travels through unstable distribution protocols.

Pace’s 2026 restructuring made the mechanism unusually visible. The gallery connected reductions in staff and roster to the correction of an expansion model it regarded as unsustainable. A decision of this scale affects artists, estates, and employees with radically different histories. Treating it as an absolute quality ranking would confuse corporate strategy with historical judgement.

The consequences for artists remain concrete. A scheduled exhibition may vanish, consigned works require return, invoices and shares require reconciliation, and collectors accustomed to a single contact need a new interface. Where representation has absorbed communication, archive, and market relations, exit produces an operational void before a symbolic one.

The contract acquires its full value at this threshold. Duration, territory, exclusivity, work inventories, insurance, reporting, payment deadlines, expense allocation, and termination procedures should be established while the relationship is healthy. An exit clause gives both sides an agreed protocol when trust is under pressure.

The most robust representation preserves a door. The artist maintains an independent archive, knows part of the professional field directly, continues conversations with curators and peers, and understands pricing mechanics. The gallery benefits from an artist able to bring opportunities, information, and relationships into the shared parameter space. Operational autonomy strengthens the alliance when transparency prevents channel conflict.

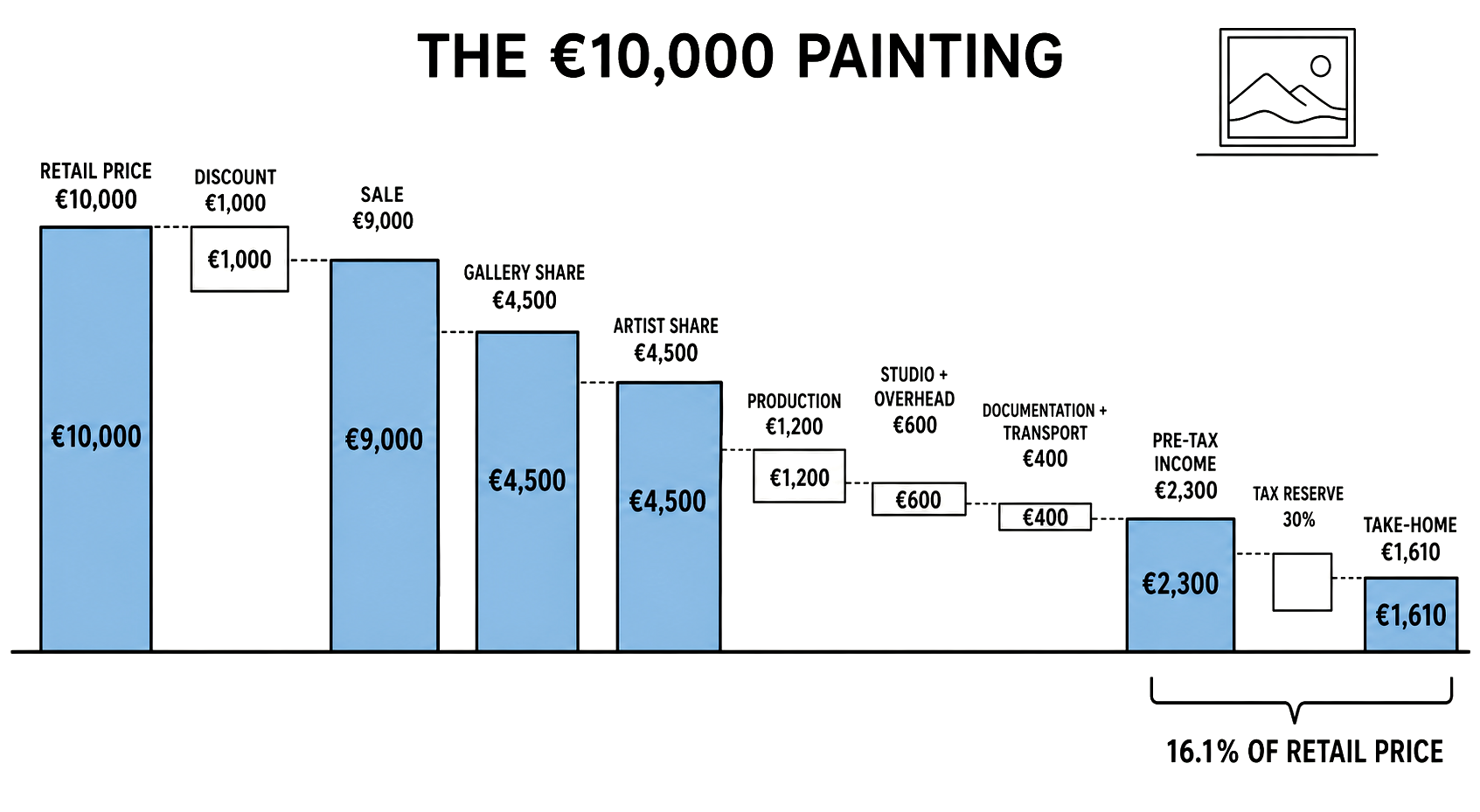

The Ten-Thousand-Euro Painting

The public price of an artwork is routinely mistaken for artist income. Consider a painting listed at €10,000. A collector receives a 10 percent discount and pays €9,000. Under a common equal split, €4,500 goes to the gallery and €4,500 to the artist. The visible figure has already undergone substantial compression before production enters the calculation.

Assume canvas, stretcher, pigment, assistance, and framing cost €1,200. Allocate €600 for studio, storage, utilities, then €400 for documentation, initial transport, packing, and administration. Professional income before tax and social contributions falls to €2,300. A purely illustrative 30 percent reserve reduces take-home income to approximately €1,610.

That €1,610 equals 16.1 percent of the original retail price. If research, testing, execution, and preparation required ten weeks, net compensation equals €161 per week. The result changes materially when the gallery advances production, deducts costs before the split, or covers transport and documentation. Commission percentage alone has less explanatory power than the full cost protocol.

The gallery’s half undergoes a parallel decompression. Its €4,500 must support staff, premises, communications, fair participation, installation, insurance, client management, and the risk of unsold inventory. Commission finances an infrastructure rather than equalling profit. Conflict emerges when service and percentage lose alignment or substantial costs remain implicit.

One sale consequently supports two interdependent economies. Price needs to include the practice’s cost, an artist margin, and the gallery’s distribution capacity while remaining within credible demand. Rapid escalation can halt sales and destabilise secondary-market sequencing; chronic underpricing leaves production structurally insolvent. Price is a promise about the future that must also fund the present.

The Income outside the Frame

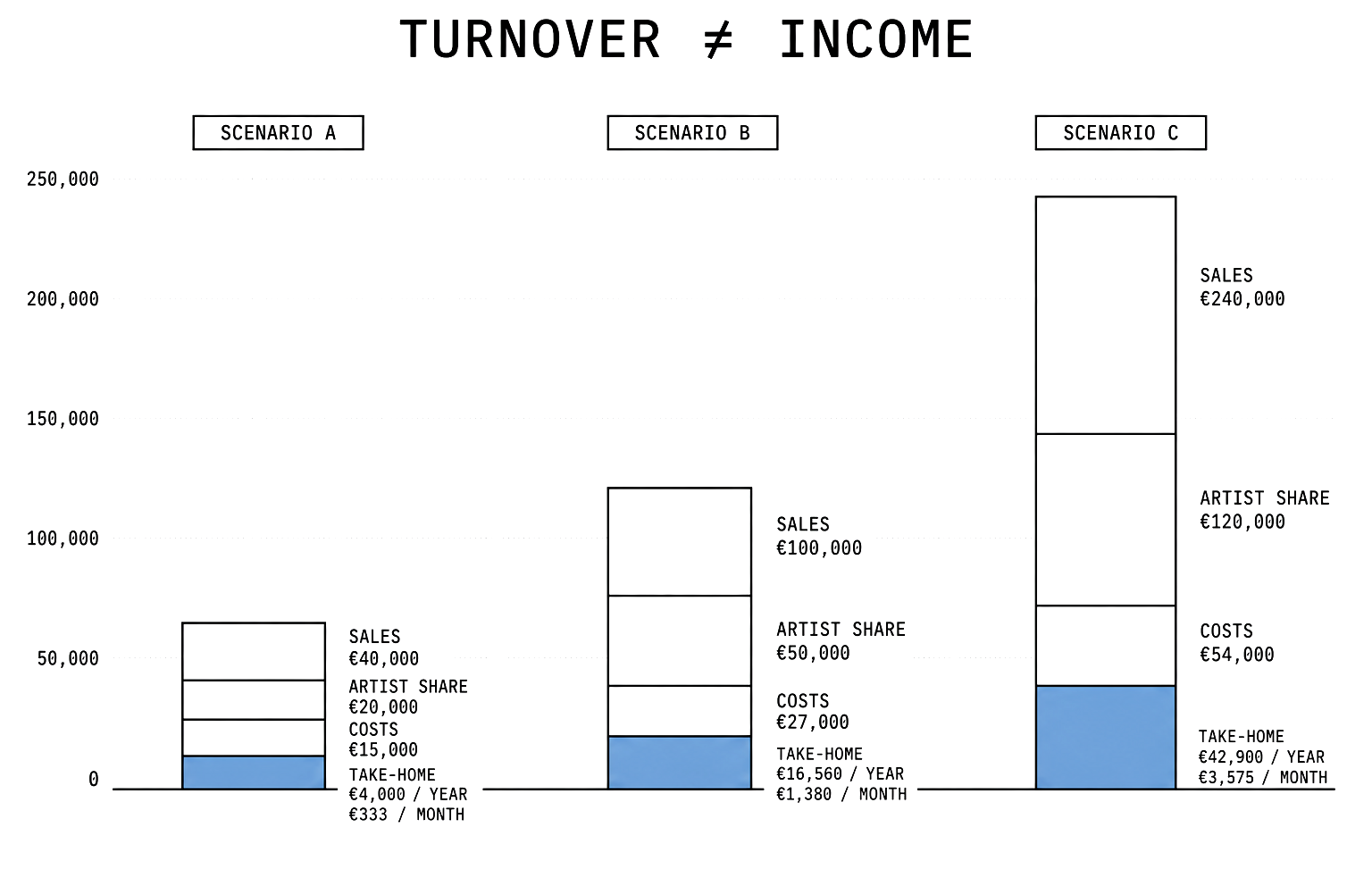

An annual simulation shows how much market turnover may be required to create an ordinary income. Three abstract European scenarios begin after discounts and before VAT, using a 50/50 division. Combined tax and social-security reserves remain illustrative modelling assumptions because national rates, deductions, thresholds, and welfare coverage occupy different parameter spaces.

In the first scenario, €40,000 in public sales leaves €20,000 to the artist. After €8,000 in production and €7,000 in studio, mobility, documentation, and administration, taxable professional income equals €5,000. A hypothetical 20 percent reserve leaves €4,000 annually, or roughly €333 per month from sales.

In the second scenario, €100,000 in sales produces a €50,000 artist share. Deducting €15,000 in production and €12,000 in structural overhead leaves €23,000. A 28 percent reserve reduces take-home income to €16,560, around €1,380 per month. Six-figure retail turnover can therefore support personal income below many conventional salaries.

In the third scenario, €240,000 in sales allocates €120,000 to the artist. After €36,000 in production and €18,000 in overhead, €66,000 remains; a 35 percent reserve produces simulated take-home income of €42,900, or €3,575 per month. The result is solid but depends on sustained demand, production capacity, and a market able to absorb yearly output at that price architecture.

Income studies explain why sales rarely stand alone. A 2024 UK survey placed median visual-artist earnings at £12,500, with more than 80 percent describing earnings as unstable or very unstable and 51 percent supplementing them through additional work. In 2024, almost one third of EU cultural employment was self-employment. An art career resembles a portfolio of intermittent income streams more closely than a salary.

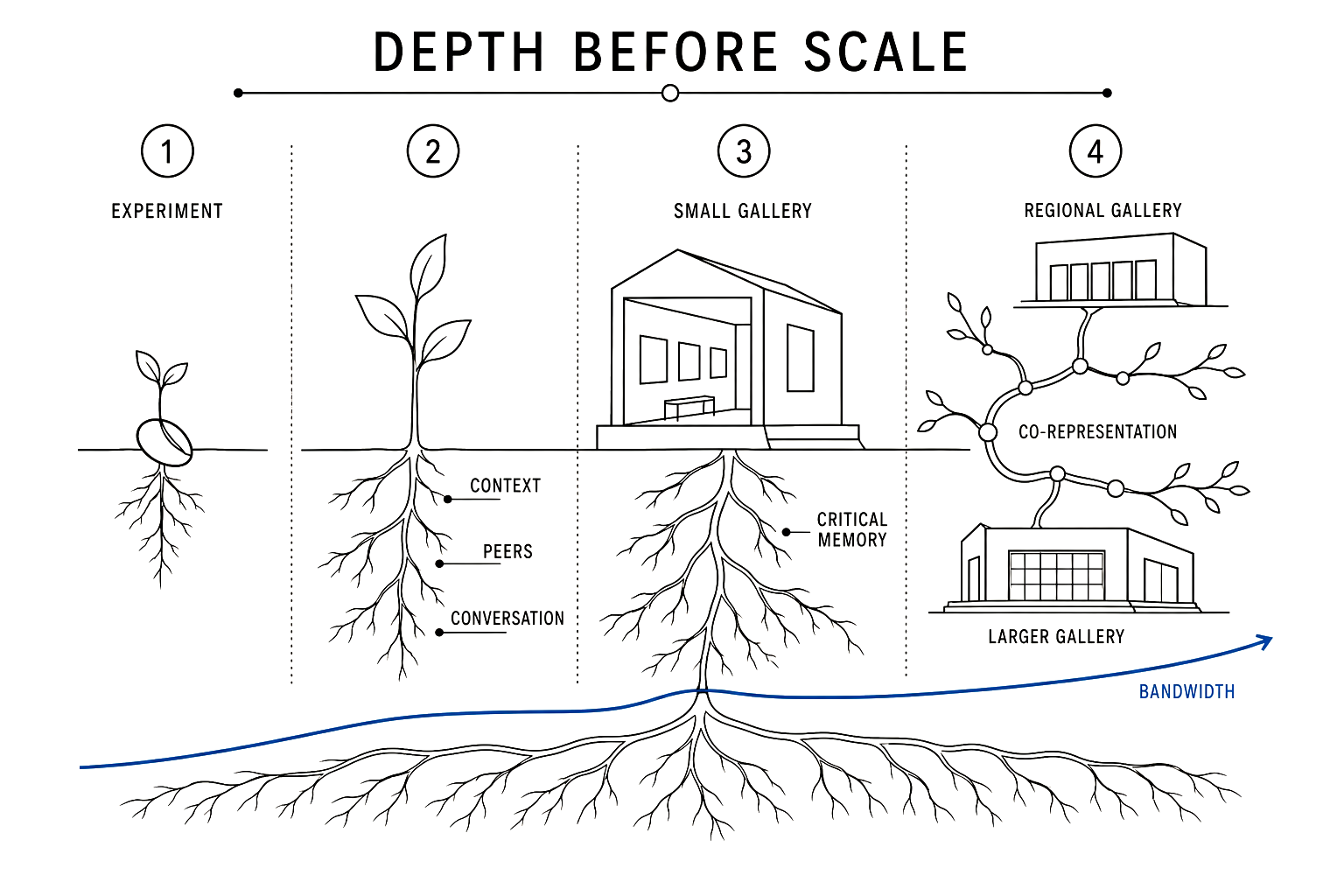

Smallness as Depth

Beginning with an independent space or small gallery can appear like a detour from the desired ranking sequence. It often provides the place where a practice learns how to exist publicly. Lower financial pressure permits experiments, failures, sharper texts, and extended conversation. The work establishes context before establishing price.

Independent spaces generate critical and social capital more readily than financial capital. They connect artists, curators, technicians, writers, and publics who share problems before sharing transactions. This network may create invitations, collaboration, and editorial attention. Its economic value often arrives later through indirect distribution protocols.

The small gallery adds a concentrated commercial relationship. It can invest a substantial part of its programme in a few artists, know buyers personally, and defend prices compatible with the practice’s development. Its constraint lies in financing costly production, international fairs, and long periods with low sales. Care and capital move through different exposure times.

Transition to a larger structure works best when it preserves this depth. Regional co-representation and gallery collaboration can expand the market while retaining the intermediary that built the first context. Such structures still require clear commission, client, and territorial protocols, yet they distribute risk and prevent growth from becoming abrupt replacement.

The choice between small and large becomes false when framed absolutely. A career may need both at different times and for different functions. Smallness contributes density, memory, and experimentation; scale contributes bandwidth, specialisation, and access. A resilient structure allows these capacities to communicate.

The Autonomous Constellation

The artist’s subsystem begins in the studio and extends far beyond its door. It includes peers who encounter the work before the market, curators who articulate context, spaces willing to absorb exhibition risk, media that establish public memory, technicians who enable production, and commercial partners able to create continuity. These relationships lose their force when reduced to instruments.

Friendship matters precisely because it exceeds networking. A friend may identify a weak exhibition, share a contact with no expected return, lend equipment, introduce a text, or remember the trajectory when market attention declines. Turning every friendship into strategy destroys it; overlooking its infrastructural capacity obscures how careers actually survive.

Media infrastructure demands equivalent care. An updated website, accurate images, a verifiable biography, accessible writing, an exhibition archive, and direct contacts create bandwidth controlled by the artist. Social platforms amplify this archive but should never replace it. Platform governance can change distribution overnight; an owned archive preserves narrative continuity.

Commercial infrastructure can remain plural while preserving transparency. Territorial galleries, public commissions, editions, licensing, architectural collaborations, agreed studio sales, and consulting may coexist when territory, percentage, and client ownership are explicit. Diversification protects income; opacity corrodes trust.

Autonomy means the capacity to continue when one node slows. It does not require the artist to perform every function, but it requires awareness of who performs it and under which terms. The constellation remains legible after one star disappears.

Rebuilding the Career Architecture

The first change concerns contract quality. Written agreements should separate sales commission, production costs, transport, discounts, promotion, and fees for talks or performances. They should establish regular accounting and a termination protocol. Clarity reduces conflict and gives gallery and artist an operational measure of reciprocal labour.

The second concerns income design. Sales, commissions, teaching, consulting, rights, editions, residencies, and public funding can form a coherent portfolio instead of a series of fallbacks. Each source needs to protect sufficient dwell time for practice. Complementary employment becomes destructive when it consumes the possibility of production.

Public policy can alter this equation. Social-security systems adapted to intermittent work, exhibition fees, resale rights, accessible insurance, and mobility support recognise value beyond the sale object. In 2026, Ireland continued its Basic Income for the Arts through a scheme funding 2,000 recipients at €325 per week for three years. The limited experiment shifts support from isolated projects toward the exposure time of practice.

Galleries are also reconsidering scale. Smaller rosters, inter-gallery collaboration, shared costs, and territorial representation can replace continuous expansion. The Art Basel and UBS Global Art Market Report 2026 recorded renewed global sales growth in 2025 alongside substantial opening, closure, and relocation activity. Growth and structural revision coexist within the same market.

The strongest art career neither hands its destiny to a gallery nor rejects galleries as a gesture of pride. It builds enough autonomy to make representation effective, enough trust to permit delegation, and enough relationships to survive separation. The contract can open a door. The constellation determines whether the route continues.